The Carbon Border Adjustment Mechanism (CBAM) is a regulatory tool that applies a price at the EU border on the greenhouse gas content of imported products, that matches the carbon price paid for similar products produced in the EU.

Its introduction is a response to concerns that increasing internal EU carbon prices risks creating a competitive disadvantage for EU producers on the European Single Market, compared to non-EU producers that don’t have to pay a carbon price. This might result in decreasing EU production or causing relocation to a country without a carbon price. Although this would reduce domestic emissions, it could result in increased emissions elsewhere. This potential outcome is known as “carbon leakage”, and its prevention was the primary reason for the introduction of CBAM within the Fit-for-55 Package.

A second key reason for the introduction of CBAM is its potential positive influence on international mitigation efforts beyond the EU. To avoid paying for CBAM, countries exporting into the EU can introduce their own carbon pricing system (with price rates matching the EU ETS), or by decarbonising their production.

Carbon leakage is the hypothetical situation where an environmental policy in one jurisdiction that leads to emission reductions, is compensated or nullified by resulting emission increases in another jurisdiction with less stringent regulations. Since the EU’s Emissions Trading System was launched in 2005, the supposed carbon leakage risk has been addressed by two main measures: free allocation of allowances and indirect cost compensation.

In reality, free allocation led to massive windfall profits and nullified any incentive for ETS sectors to decarbonise their production. Only the electricity sector, because it was combusting fossil fuels, was required to purchase most of its allowances in auctions from 2013 onwards. Other emission-intensive industries such as those manufacturing steel and iron, cement and aluminium, received the majority of their allowances for free and incredibly pocketed even more than they required throughout the lifespan of the EU ETS.

Indirect cost compensation allows member states to redress industries for increased energy costs passed through by the electricity sector.

However, the compensation has removed an incentive for the affected companies to decarbonise their production or to increase their usage of renewable energy sources. As free allocation rules were updated to accommodate the introduction of CBAM, a recital of the Regulation stipulates that indirect costs compensation rules be updated to allow indirect emissions to be accounted for all CBAM products. As indirect emissions become integrated within the scope of CBAM, the indirect cost compensation should also be phased out.

The intention of CBAM is to reflect the EU ETS price as closely as possible. In addition to shielding industrial actors from economic disadvantages, it will set and maintain a carbon price that incentivises emission reduction. In order to comply with international trade law, CBAM must mirror the price of EU ETS allowances. To unleash its full potential there must be an end to free allocation.

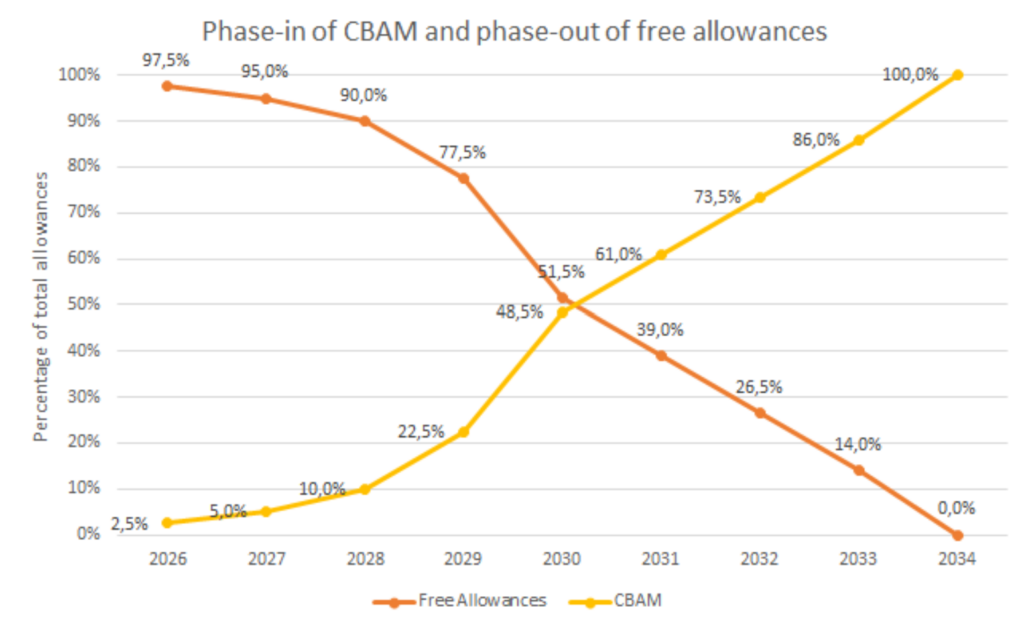

The figure below shows the agreed time plan for the phasing out of free allocation and the phasing in of CBAM.

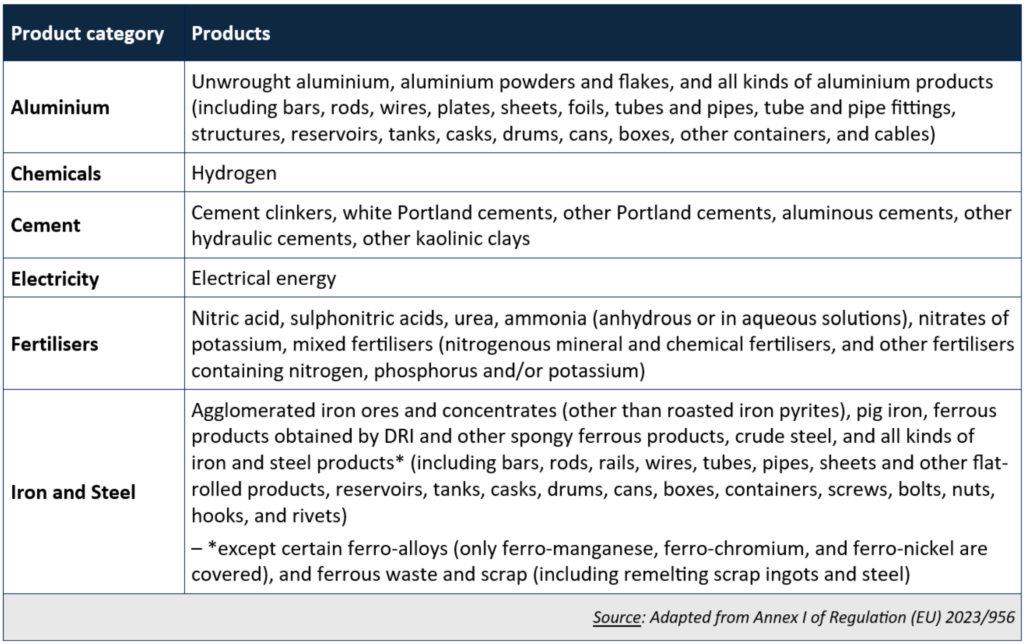

CBAM will cover imported cement, iron and steel, aluminium, fertilisers, electricity and hydrogen, arriving from outside the EU. For each sector a list of classified products has been selected based on Combined Nomenclature (CN) codes.

More products (e.g. chemicals such as plastic polymers) should be included to increase CBAM’s effectiveness for emission reduction.

In addition to defining the general product scope, policymakers attempted not only to cover the immediate end products of these sectors but also precursors (e.g. ferroalloys for steel production) and products down the value chain (e.g. screws) in order to prevent circumvention. Nevertheless, significant gaps remain. Covering all relevant precursors under CBAM will ensure an end to the free allocation of allowances for these industries too.

CBAM covers both direct and (only for cement and fertilisers) indirect emissions. Direct emissions are released during the production – and are defined as Scope 1. Indirect emissions refer to emissions occurring from the electricity used during production, and are described as Scope 2 emissions. Direct and indirect emissions of relevant precursors (the raw materials used in the production of complex goods) are also taken into account when calculating the carbon intensity of CBAM products. A typical example of a precursor is cement clinker, which is the main constituent of ‘Portland cement’.

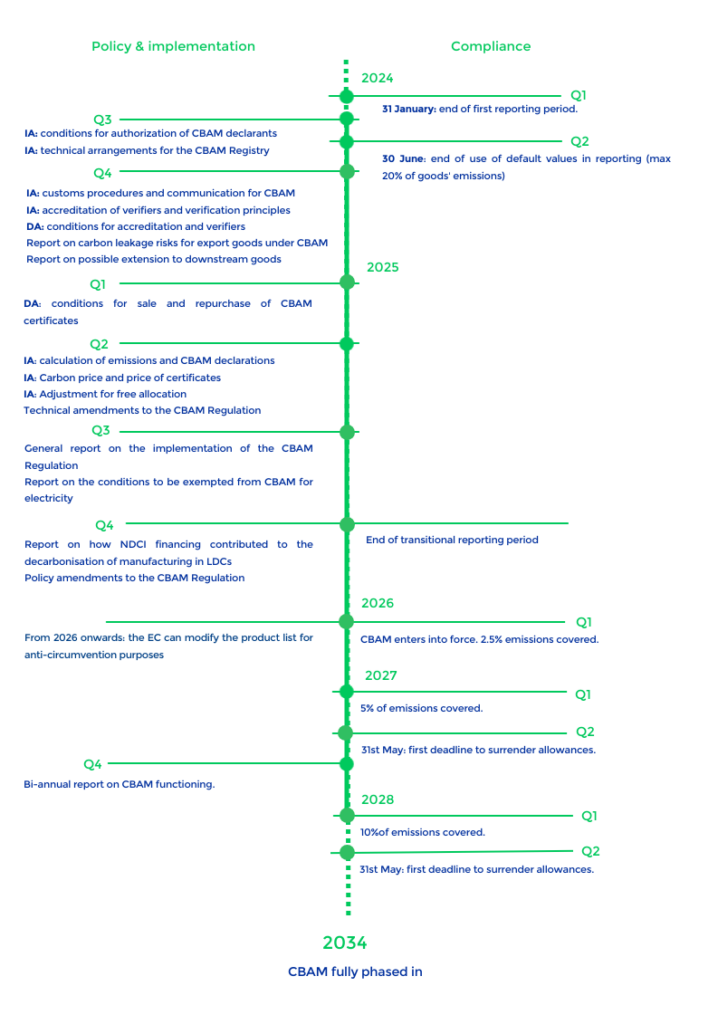

Transitional monitoring period

Starting in October 2023, a transitional two year monitoring period requires importers to submit quarterly reports for CBAM goods (accounting the direct and indirect emissions for all products) to the European Commission following the methodology explained in ‘4. How are emissions calculated under the CBAM?’. The monitoring period brings an opportunity for policymakers to fine-tune the regulation to avoid circumvention, plan future scope enlargement, and build capacity at national level for the definitive phase-in during 2026.

Monitoring & Reporting

Importers are entitled to import CBAM goods once they have been granted an authorisation by the competent authorities responsible for the application of the CBAM Regulation. These authorities are designated and managed by member states. The European Commission can advise and assist the authorities in carrying out the activities required by the CBAM Regulation.

The Commission will establish the CBAM Registry, a standardised electronic database containing data regarding the CBAM certificates of authorised CBAM declarants. All information will be automated and made available in real-time to competent authorities. The application for an authorisation should be submitted via the CBAM registry.

Each authorised importer or representative has to submit a CBAM declaration, by 31 March of each year, detailing the total quantity of goods imported in the previous year, the total embedded emissions per tonne of each type of goods and the number of certificates – corresponding to the total embedded emissions – that must be be surrendered.

Verification

The authorised importer has to ensure that the emissions declared upon importation are verified by an accredited verifier based on set verification principles. Accredited verifiers carry out verification reports based on principles laid out in Annex VI – assessing that there are no misstatements in the reports. Installation visits are to be carried out unless there are specific reasons not to do so.

The European Commission ensures alignment of qualifications between verifiers and tasks through an implementing act. The Commission also oversees the review of CBAM declarations.

Buying and surrendering

Companies that want to import goods produced outside the EU into the EU must purchase certificates corresponding to the amount of emissions generated in the production of those goods and surrender them on a yearly basis.

The European Commission will calculate the price of CBAM certificates to reflect the average weekly price of ETS auctions. This means that CBAM certificates will be pegged to the ETS. This will fix the price of CBAM certificates as close as possible to the price of ETS allowances while also ensuring that the system remains manageable for the administrative authorities. For products from sectors receiving free allowances in the EU only a corresponding fraction of emissions has to be paid for by purchasing CBAM certificates.

There is no limit on the number of CBAM certificates an importer may purchase to avoid imposing restrictions on trade. Unlike ETS allowances, CBAM certificates are neither tradeable nor bankable to ensure they constantly reflect the evolution of the ETS price. Any divergence could create disparities in price and either weaken the incentives for decarbonisation or lead to violations of international trade law (e.g. article III:4 GATT).

Certificates are valid for two years from the date of purchase. Re-purchasing is the only form of “transaction” allowed on CBAM certificates. An importer can re-sell its certificates in excess – up to a third of the total certificates purchased the year before – to the competent authority. This should preserve some flexibility and the possibility for importers to optimise their costs without undermining prices or introducing speculation into the system.

Default values

For part of the transitional reporting period, CBAM declarants used global default values as set by the European Commission with the support of the Joint Research Centre. For the definitive period, the Commission will set default values by country (and even by region) informed by the data collected during the transitional reporting period. Otherwise, “best available data” based on reliable and publicly available information will be used, and revised periodically through implementing acts, according to Annex IV (4).

Actual emissions

For industrial products, Annex IV (2-3) lays out the calculation methodologies of embedded emissions – taking into account the total emissions of goods (simple or complex) and the activity level (quantity of goods produced) during the reporting period.

Due to the increased risk of circumvention related to electricity , stricter “conditionalities” are to be met when reporting actual emissions values in its import, as described in Annex IV(5):

- The amount of electricity is covered by a power purchase agreement between the CBAM declarant and a producer of electricity located in a third country;

- The installation producing electricity is either directly connected to the EU transmission system, or it can be demonstrated that at the time of export there was no network congestion at any point in the network between the installation and the EU transmission system;

- The producing installation does not emit more than 550 g of CO2 of fossil fuel origin per kWh of electricity;

- The amount of electricity has been nominated to the allocated interconnection capacity by all responsible transmission system operators in the country of origin, the country of destination and each country of transit, and the nominated capacity and the production of electricity by the installation refer to the same period of time, which shall not be longer than one hour.

Article 7 of the Regulation empowers the Commission to adopt implementing acts to flesh out the details of these methodologies.

The proposal includes three types of exemptions:

- Countries outside the EU but participating in the EU ETS, and countries with carbon markets linked to the EU ETS are excluded from CBAM (EEA countries, Switzerland).

- In the case of countries with comparable carbon prices, an importer will be allowed to claim a reduction in the number of CBAM certificates to be surrendered corresponding to the carbon price already paid in other jurisdictions

- The Regulation accepts reductions when a carbon price has been “effectively paid”. To assess effectiveness, any rebates or compensations shall be taken into account. The European Commission is expected to provide further guidance through an implementing act in 2025.

- If a third country has an electricity market that is integrated with the EU internal market for electricity through market coupling, and it has not been possible to find a technical solution for applying the CBAM to electricity imports in the EU, the importation of electricity from the country will be exempted from the application of the CBAM, provided certain corresponding conditions are satisfied.

- Finally, the “force majeure” clause in Article 30 states that where an unforeseeable, exceptional and unprovoked event has occurred that is outside the control of third countries subject to the CBAM, and that event has destructive consequences on their economic infrastructure, the Commission shall submit a report to the co-legislators, accompanied, where appropriate, by a legislative proposal setting out the necessary provisional measures to tackle the situation.

- This provision is likely to be triggered ahead of the start of the definitive period to avoid hindering Ukrainian imports.

According to the Regulation, member states have the responsibility to collect the revenues arising from selling CBAM certificates. Based on these revenues, the European Commission presented a proposal for a CBAM-based own resource..

75% of total CBAM revenues (an expected €1.5 billion per year starting in 2028) would be available, but at the time of writing there is no indication of how that money will be spent. Several experts, as highlighted in an European Parliament own initiative report, have raised concerns about reinvesting this money back into European industry, which would put the CBAM at risk of breaking compliance with WTO rules.

Moreover, several stakeholders, based on research that forecasts potential negative impacts of the CBAM on developing economies, recommend that CBAM revenues should be reinvested towards climate change mitigation and adaptation in those countries as a contribution towards the broader objectives of the Paris Agreement and compliance with the Common But Differentiated Responsibilities and Respective Capabilities (CBDR-CR) principle.

DA: Delegated Act

IA: Implementing Act

Based on the European Commission’s timeline from the CBAM Expert Group.