The EU Emissions Trading System (EU ETS) is often referred to as a cornerstone of EU climate policy. It aims to reduce emissions by pricing greenhouse gas (GHG) pollution from the power, heavy industry, aviation and maritime sectors. Buildings and road transport will be included in a separate ETS2 from 2027. The EU ETS seeks to promote investments in emission reductions by making energy-intensive business as usual more expensive. The EU ETS seeks to apply the ‘polluter pays’ principle by making companies bear more of the climate cost of their carbon emissions. It also offers a great opportunity for the EU to shift funding from polluting activities to climate action, innovation and energy sector modernisation.

The EU ETS covers more than 10,000 industrial and power installations and airlines operating flights in and between EU airports only, across the 27 EU member states, Iceland, Norway and Liechtenstein (there is a link with the Swiss ETS). In 2013, the EU ETS covered approximately half of all EU’s GHG emissions. From 2023, the system covers about 36% of the bloc’s emissions, with this shrinkage a result of emissions reductions of 37.3% below 2005 levels in the heavy industry and power sectors.

Agreed in 2023, the new ETS target to reduce emissions from the original sectors covered is raised to 62% by 2030 compared to 2005 levels. When the ETS2 is introduced, roughly three-quarters of the EU’s emissions will be covered by the scheme. The ETS2 aims to bring emissions in buildings and road transport down by 42% over the same period.

The EU ETS is a ‘cap and trade’ system. This means that it sets an overall limit (a ‘cap’) on the total volume of greenhouse gas (GHG) emissions that installations in the covered sectors can collectively emit. The reduction targets set by EU policymakers are achieved through the gradual lowering of this cap.

The cap is divided into pollution permits known as EU Allowances (EUAs). One EUA represents one tonne of CO2 equivalent emissions. In 2022, the cap was approximately 1.52 billion EUAs.

Companies can buy and sell allowances, including those they received for free, on the open market and trade them with each other. This is what the ‘trade’ part in ‘cap and trade’ refers to. For example, if a company has succeeded in lowering its emissions particularly fast, it can sell its spare allowances to another company or save them for future needs – this is called ‘banking allowances’. This trading element is the part of the EU ETS that should, in theory, enable cost-efficient decarbonisation by allowing companies with high decarbonisation costs to buy permits from companies with lower costs.

Installations covered by the EU ETS are obliged to hand over (also known as surrender) EUAs equal to their emissions of the previous year. For example, an installation that emitted 1 million tonnes of CO2 in 2023 would need to transfer 1 million EUAs to the European Commission’s central registry in 2024. If the company fails to do so, they will need to pay a fine on top of the price of each allowance to be surrendered.

Companies can acquire EU Allowances (EUAs) through three main channels:

- Buy them at auction: auctions are organised by the European Energy Exchange, with the revenues going directly to the EU’s 27 member states according to a predefined division key.

- Receive them for free: sectors deemed to be at risk of carbon leakage, the aviation sector, and electricity producers in some lower-income member states receive free allocations. In 2022, more than 89% of industrial climate pollution was subsidised via free allowances at no cost to industry but at enormous cost to the environment and society.

- Buy them on the open (or so-called secondary) market: there are several trading platforms where ETS operators (or others such as financial institutions) can trade allowances. Transfers of EUAs can also be included in other contracts (for example, for the purchase of heat or electricity).

“Carbon leakage” refers to a hypothetical situation where companies transfer their production, or parts of it, to countries with weaker climate policies to lower their production costs. This risk has yet to materialise due to carbon pricing, but this concept has shaped the design of the EU ETS since its inception.

Free allocations of pollution permits are meant to shield companies from the perceived risk of carbon leakage. The European Commission compiles a ‘Carbon Leakage List’ of sectors that receive 100% of their allowances for free up to a benchmark level. This means that the relatively most efficient plants receive all of their allowances for free, while the least efficient ones get 30%.

The falling cap on emissions is enforced through limiting the supply of pollution permits, or EU Allowances (EUAs): each year only as many EUAs are made available through auctions and free allocations for companies as the cap for that year. The cap is reduced each year, to ensure GHG emission from the involved sectors decrease as well. Companies are aware that, in theory, this means that EUAs will become increasingly scarce and costly over time.

The anticipated rising cost of acquiring an EUA in the future is meant to give companies an assumed financial incentive to reduce emissions. Either these companies pay to continue their high emissions, or they invest in technologies and other means to reduce their emissions.

However, this presumes a high enough carbon price to disincentivise emissions. Historically, the EU ETS has suffered from low prices on pollution due to a glut of pollution permits on the market. These low prices undermined the core objective of the EU ETS. However, confidence in the EU ETS has been surging since the most chronic oversupply issues started to be addressed in 2018, leading to more accurate and fairer carbon prices. Nevertheless, these supply issues have only partially been resolved, with the oversupply standing at about 1.13 billion pollution permits in 2022. In early 2024, prices have again tumbled, undermining the ETS’s effectiveness as a decarbonisation policy instrument and a source of revenue for climate action.

There are two main mechanisms that determine how many EUAs are supplied each year: the linear reduction factor (LRF) and the market stability reserve (MSR).

For 2024, the EU ETS’s cap stands at 1.39 billion pollution permits, or EU Allowances (EUAs), allowing emissions of 1.39 billion tonnes (or 1.39 gigatonnes, Gt) of CO2e. For comparison, environmental NGOs estimate that the total carbon budget available to the EU stands at approximately 27.5 GtCO2 for the period 2020-2050, which translates as less than a gigatonne a year. This means that, despite its aspirations, the EU ETS in 2024 covers more than the entire carbon budget for the EU this year, even though the ETS only represents less than half of the bloc’s emissions.

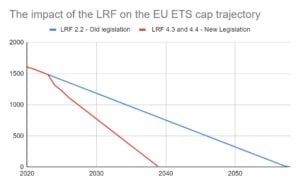

The EU ETS cap decreases by a fixed amount each year, which is calculated using the so-called linear reduction factor (LRF). The LRF is expressed as a percentage of the 2013 total cap.

For 2013 to 2020, the LRF was set at 1.74%, or about 34 million EU Allowances (EUAs) a year, and starting in 2021 it is set at 2.2% (about 43 million EUAs a year).

There is a direct correlation between the LRF and climate ambition: the higher the LRF, the lower the emissions. Unsurprisingly, the size of this factor has become a central issue in negotiations around reforming the EU ETS. The last agreed revision of the EU ETS has further increased this factor: the LRF is set to 4.3% from 2024 to 2027 and 4.4% from 2028 to 2030.

So while the LRF may appear small, it is crucially important for the functioning and ambition of the EU ETS. It sets the supply of EUAs, determines the available decarbonisation pathways and the total carbon budget. This means that the LRF has a massive impact on the environmental integrity of the ETS and the behaviour of the companies governed by it.

The oversupply of EU Allowances (EUAs) exceeded 2 billion in 2013. Due to this saturation, the EU carbon price sank to as low as €5 a tonne of carbon. Such a low carbon price undermined confidence in the EU ETS as an effective scheme to reduce emissions. A volume-based mechanism, known as the Market Stability Reserve (MSR), was introduced to combat this oversupply, functioning according to predictable and objective parameters. When it was activated in 2019, the period of ultra low carbon prices ended.

The MSR is a supply control mechanism that can limit the number of allowances in circulation. It works on an annual cycle. Each year, the European Commission calculates the ‘total number of allowances in circulation’ (TNAC) – which in essence represents the oversupply under the EU ETS. The TNAC represents the number of allowances that left the market minus the number of allowances that have entered the market. If this quantity is greater than 833 million, a percentage of the oversupply is transferred to the MSR. The TNAC for 2022 totalled 1.13 billion allowances, still well in excess of the threshold of 833 million.

The mechanism plays a major role in regulating oversupply. Over 272 million allowances are due to be removed between September 2023 and August 2024.

Although we are currently still in a period of oversupply, the MSR is also designed to play a role in the so-far hypothetical case that the EUAs in circulation are considered too few for market functioning and liquidity. If the oversupply is lower than 400 million, the market is considered by policymakers to be ‘too tight’. If this occurs, the following year an additional 100 million EUAs will be withdrawn from the MSR and auctioned.

The Market Stability Reserve has proven effective in supporting the carbon price. However, the MSR was only designed to tackle the historical oversupply, which will take years to absorb. It is not fit to deal with current or future surpluses or shocks.

For example, current national coal phase-out plans could add another 2 billion EUAs to the oversupply between 2021 and 2030. The MSR needs to be bolstered if this and other additional oversupplies are to be kept from sinking the carbon price again.

While the EU ETS’s central goal is to reduce emissions, it has a co-benefit of generating significant revenue through the auctioning of pollution permits or EU Allowances (EUAs), despite the fact that most allowances to industry are handed out for free. These funds are a huge opportunity to finance climate action and support people through the climate transition.

Since its inception in 2005, the EU ETS has raised over €152 billion in revenue for member states. This amount was increasing rapidly due to rising carbon prices, even as the cap decreases, however it varies due to the forces of market demand and supply. In 2022, income amounted to €38.8 billion, €7.7 billion more than in 2021.

However, ETS revenue could have been much higher if it were not for free allocations to industry and airlines. It is estimated that between 2021-2030, the ETS will allocate about 5 billion allowances for free. Assuming a €80 per tonne carbon price, this represents €400 billion in foregone auctioning revenue, a missed opportunity to fund much-needed climate action.

A large portion of the revenue from the EU ETS goes directly to member states, while some of it is channelled through other instruments that seek to stimulate innovation or finance a just transition. Some 425 million EU Allowances (EUAs) between 2023 and 2030 will go to the Innovation Fund, which supports the development of low-carbon technologies. In addition, €57 billion worth of allowances will be allocated to the Modernisation Fund between 2021-2030, assuming a carbon price of €75 per tonne. The Modernisation Fund assists 13 lower income member states to modernise their energy sectors and improve energy efficiency.

Following the latest ETS revision, all of the remaining revenue allocated to member states must be earmarked for ‘climate action’. However, this is a non-binding recommendation, and EU countries are free to ignore it, though they have to report on their revenue use. The list of activities on which the ETS revenues can be spent is broad and gives leeway to use ETS revenue to write off regular national spending. Additional guidance is required for member states to ensure spending achieves the needed emissions mitigation.

Member state reports to the European Commission show that the majority of revenue labelled as climate spending supposedly goes to promoting renewables and energy efficiency. However, this is doubtful because the reporting is vague and of very low quality, with some countries leaving most or everything of the reporting template empty. Moreover, some spending has clearly been going against the ethos of climate action (and may even hamper the accomplishment of climate goals). For example, in 2021, Germany and Belgium spent 7% and 9% of their revenues on subsidy schemes compensating industry for indirect costs, while Poland and Hungary spent €11.6 million and €25.2 million of their respective ETS revenues to fund fossil fuel heating systems.

Looking forward, the new ETS2 for buildings and road transport is expected to raise an additional €260 billion in revenue from when it launches in 2027 to 2032, assuming an average price of €45 per tonne. It is vital that the permitted avenues for the spending of ETS revenue is clearly defined before the ETS2 launches. The limited ETS2 revenue must be used to combat the risk of increased energy poverty and provide affordable access to emissions reductions across buildings and road transport.

If you would like to learn more about how the EU ETS works you can find more information here:

- EU ETS 101 guide

- FAQ: CBAM FAQ

- FAQ:The EU ETS for Shipping Explained

- FAQ: The EU ETS for Aviation Explained

- Free Allocation Regulation (FAR)

- Enhancing EU climate action before and after 2030 – the role of the EU ETS and carbon removals

- The Emissions Aristocracy

- Can the EU’s Expanded Emissions Trading System Ensure a Just Transition for Vulnerable People and the Climate?